4.3 CAPM

In a competitive market, a security is supposed to provide an expected return commensurate with its systematic risk the risk that can't be avoided by diversification. The greater systematic risk of a security, the greater return that investors will expect from the security. The relationship between expected return and systematic risk, and the valuation of securities that follows, is the essence of the capital asset pricing model(CAPM), which was produced by William Sharp, John Lintner, and Jack Treynor in 1960s. This model has had important implications for finance ever since. Though other models also attempt to capture market behavior, the CAPM still remains popular due to its simplicity and utility in a variety of situations.

4.3.1 CAPM Assumptions

資本資產定價模型(Capital Asset Pricing Model簡稱CAPM),主要研究證券市場中資產的預期收益率與風險之間的關系。

Any economic model is a simplification of reality. No exception, the CAPM rests on the following assumptions:

· Investors are rational utility maximizers, all investors have similar expectations.

·Capital markets are efficient in that investors are well informed, tax and transactions costs are low, and information is freely available.

·Investors can borrow and lend at the risk free-rate.

· Investors hold diversified portfolios-market portfolio, thereby eliminating all unsystematic risk.

As we said early, market portfolio is the portfolio of all assets in the economy. In practice a broad stock market index, such as the S&P 500 Composite , Shanghai composite index in China, is used to represent the market. Obviously such market portfolio has a beta of 1.0.

, Shanghai composite index in China, is used to represent the market. Obviously such market portfolio has a beta of 1.0.

4.3.2 Risk and Return Under CAPM

風險資產的收益率=無風

It is commonly acknowledged that the least risky investment is government bond, generally say, U. S. treasury bills, which offer fixed return and will be unaffected by the market. In other words, treasury bills have a beta of 0. We can assume that it is risk-free investment. We also considered a much riskier investment, the market portfolio of all securities, with beta of 1.0. Investors require a higher return form risky investment than from the risk-free investment. Required rate of return

險收益率+風險溢價

市場風險溢價:市場平均收益率超過無風險收益率的那部分。

=Return from risk-Free investment+Risk premium

If the investors hold market portfolio, they will require return ofRm that is higher than the risk-free security, the excess return of the market portfolio is termed the market risk premium:

Market risk premium=Rm-Rf

For any risky asset i, CAPM describes the relationship of risk and return as

Ri=Rf+βi(Rm-Rf)

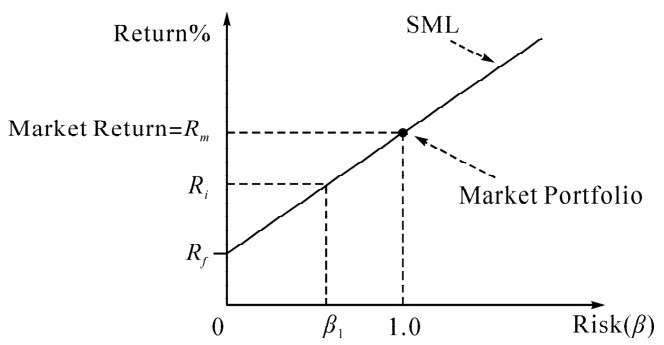

證券市場線

When graphed, CAPM equation is called the security market line and is illustrated in Figure 4.4.

Figure 4.4 Security Market Line

CAPM theory suggests that each risky asset should plot along the line. The expected return on a risky asset consists of two components:the risk-free rate of return plus a premium for risk. The risk premium for each asset depends on the asset's beta(βi)and on the market risk premium(RmRf).

Illustration 4.3

Equity beta of British Airway:1.65

Risk-free rate(yield on Treasury bills):2%

Market average return:7.0%

Thus, market risk premium=7.0%-2.0%=5%

Ri=2%+(1.65×5.0%)=10.25%

This represents shareholders' required rate of return and hence the cost of equity of British Airways.

4.3.3 Implication of CAPM

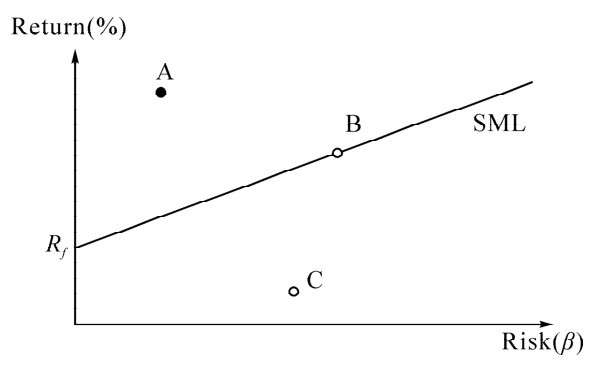

The CAPM provides us a means to estimate the required rate of return on a security. It takes into account the asset's sensitivity to market risk(represented by beta), risk-free rate of return and expected return of the market. It shows the required rate of return on risky security(asset price), as well as the cost of equity, should be determined by beta. SML essentially graphs the results from CAPM(Figure 4.5). If the security's expected return versus risk is plotted above the SML, it is undervalued since the investor can expect a greater return for the inherent risk. And a security plotted below the SML is overvalued since the investor would be accepting less return for the amount of risk assumed.

Figure 4.5 Risk and Return

CAPM has been argued ever since it was born. Despite it failing numerous empirical tests, and other emerging modern approaches(such as arbitrage pricing theory), the CAPM still remains a practice way to look at risk and return that might be required in capital market.